Search

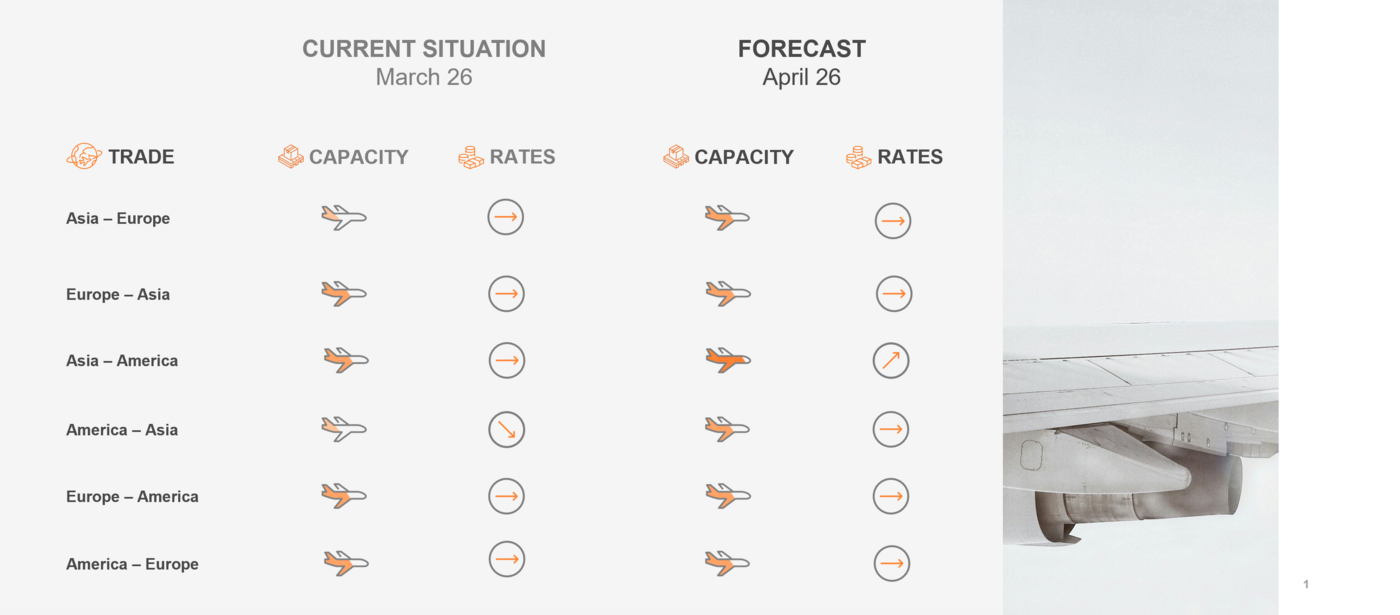

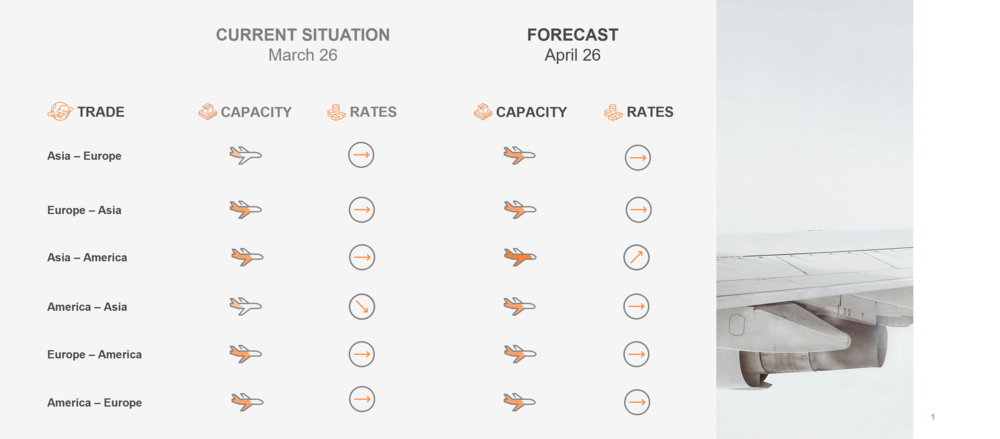

Reliable air freight planning requires up-to-date market information. Our monthly Air Freight Market Update offers a concise overview of rate developments, capacity availability, and other relevant market changes.

| Global Air Cargo forecast 2026 | WACD expects a tonnage increase by 2,70% and IATA air cargo traffic ist projected to grow by 2,60% and cargo increase by 2,4% |

| Sustainable Fuel | Global production of Sustainable Aviation Fuel (SAF) continues to rise and is expected to reach 2,4 million tonnes in 2026. However, SAF is still projected to account for only 0,80% of global jet fuel consumption by 2026. |

| Market driver | Asia Pacific, the Middle East and South Asia are expected to drive industry growth, together accounting for more than half of global air cargo volumes. |

| Air Cargo Capacity | Air cargo capacity is expected to continue growing and may outpace demand growth in 2026. Capacity expansion has been driven mainly by belly capacity, while freighter capacity remains under pressure on certain trade lanes. |

| Spot-air cargo rates globally | From today´s perspective, spot air cargo rates are expected to remain at similar level to 2025, with regional and seasonal fluctuations. |

For further insights or shipment-specific guidance, speak with one of our local specialists.

WACD expects an overall air cargo tonnage increase by approximately 2,80% in Q1 2026.

What this means for shippers

Early planning remains essential for main deck and project cargo. Spot opportunities exist on several lanes.

Flexible routing and booking windows will help secure competitive rates.

Geopolitical situation

The U.S. Supreme Court has nullified key tariff policies, disrupting established economic strategies. US President Donald Trump has said he will impose global tariffs of 15%, as he has continued to rail against a Supreme Court ruling that struck down his previous import taxes.

Meanwhile, U.S.-Iran negotiations are facing new, intense scrutiny due to escalating regional pressures.

Russia is expanding "gray zone" warfare in Europe to increase the costs of supporting Ukraine